Medicare Made Simple

Medicare is the primary provider of medical coverage for Americans 65 years and older. Navigating health-care in retirement can be convoluted and stressful, and it is critical you obtain the best Medicare coverage to meet your needs, so you can maximize your health benefits and minimize your health-care costs. With these challenges in mind, check out our session with Chapter, a leading Medicare advisory company, along with our breakdown of the four-part Medicare program.

Medicare: The Four-Part Program

Medicare, a Four-Part Program is the primary provider of medical coverage for American seniors. The program’s mission is to help provide healthcare coverage to U.S. citizens who are age 65 and older and who have qualifying disabilities. Medicare is a four-part program that involves the following:

- Part A - Hospital Insurance

- Part B - Medical Insurance

- Part C - Medicare Advantage Plans

- Part D - Prescription Drug Coverage

Part A - Hospital Insurance

Part A can be viewed as hospitalization coverage. In general, this part helps cover in-patient care in hospitals, skilled nursing facility care, hospice care, nursing home care (inpatient care in a nursing facility that is not custodial or long-term care), and home health care. To qualify, you or your spouse must have worked and paid Medicare taxes for a minimum of 10 years. Note that most people do not pay a premium for Medicare Part A; however, deductibles and coinsurance – the percentage of the cost of a covered healthcare service you pay after you have paid your deductible – do apply. The Part A deductible for 2024 is $1,632 for each benefit period. The benefit period is how Medicare measures your use of medical services. A benefit period begins the day you are admitted as an inpatient and ends when you have not received inpatient care for 60 consecutive days. You must pay the deductible for each benefit period, and there is no limit on the number of benefit periods you can have.

Part B - Medical Insurance

If you are eligible for Medicare Part A, you are also eligible for Medicare Part B, which helps cover medically necessary equipment and services. In other words, Part B provides outpatient and medical coverage. Items that fall under Part B coverage include services from doctors and other healthcare providers, lab work, x-rays, outpatient care and surgeries, home healthcare, ambulance services, medical equipment like wheelchairs, walkers, and hospital beds, and preventative services like disease screenings, shots and vaccines, and annual wellness visits. For 2024, the Part B premium is $174.70, and deductibles and coinsurance apply. Note that individuals who earn more than $103,000 per year ($206,000 for a couple) are required to pay more for Part B.

Part C - Medical Advantage Plans

I’m covering Part C last because it is somewhat of its own plan. You must be eligible for Medicare Part A and Part B to be eligible for Medicare Part C, which is also known as Medicare Advantage. Medicare Advantage is a Medicare-approved plan from a private company that offers an alternative to Original Medicare, the latter referring to Medicare Part A and part B. Because Medicare Part C plans are offered by private insurance companies approved by Medicare, these plans work similarly to other private health insurance plans. With Medicare Advantage Plans, you are often required to use doctors in your plan’s network. People opt for Medicare Advantage because such a plan may have lower out-of-pocket costs than Original Medicare and reduce the costs of purchasing services separately. Medicare Advantage Plans also offer additional benefits that Original Medicare does not like coverage for hearing, dental, vision services, and prescription drug coverage. However, Medicare Advantage Plans put an annual cap on out-of-pocket expenses, unlike Original Medicare, and these plans restrict you to a smaller, local network of doctors and healthcare providers. Although people tend to select a Medicare Advantage Plan because it covers more benefits than Original Medicare (Part A and Part B), the extra coverage comes at a price. Individuals cannot opt out of Original Medicare, so if you go with a Medicare Advantage Plan, you will need to continue paying the premiums for Part A and Part B on top of your Part C premium.

Part D - Prescription Drug Coverage

Medicare Part D helps cover the cost of prescription drugs, including many shots and vaccines. Participants pay for Part D plans out-of-pocket and are required to pay monthly premiums, and annual deductible, and copayments for certain prescriptions. These costs vary by plan. You join a Part D plan in addition to Original Medicare or you can obtain Part D coverage by joining a Medicare Advantage plan with drug coverage. If you are enrolled in a Medicare Advantage Plan, you will only need to consider Part D coverage if your plan does not include it.

Medicare: Enrollment

It is important to note that if you are already claiming Social Security benefits, you will be automatically enrolled in Original Medicare, Medicare Part A and Medicare Part B, upon turning age 65. Otherwise, you can sign up during your Initial Enrollment Period, which is a seven-month period that starts three months before your 65th birthday, includes the month of your 65th birthday, and ends three months following your 65th birthday. If you miss your Initial Enrollment Period, you can register during the General Medicare Enrollment Period, which is January 1 to March 31 every year, and your coverage will start on July 1. You may also be eligible for a Special Enrollment Period if you have had a certain qualifying life event. If you miss these enrollment opportunities, you will most likely have to wait for the annual Medicare Open Enrollment Period in the fall. It is during this annual Medicare Open Enrollment Period that you can make Medicare coverage changes that involve switching and/or adding/dropping plans.

Medicare vs. Long-Term Care

Medicare does not cover long-term care – often called custodial care, meaning non-medical care that can be provided by non-licensed caregivers. Most nursing home care is custodial – in other words, non-medical – care, which is care that involves assistance with daily living activities like dressing, eating, using the bathroom, personal hygiene and bathing, and mobility. Most long-term care is not medical care; however, some long-term care is known as skilled care that can only be provided by or under the supervision of skilled or licensed medical professionals. Although Medicare does not cover long-term nursing care, Medicare does help pay for recovery in a skilled nursing care facility after a minimum of a three-day hospital stay. Medicare will cover the total cost of skilled nursing care for the first 20 days, after which you must pay a daily coinsurance, which typically involves Medicare paying 80% of the cost and you paying 20% of the cost for the next 80 days. Skilled nursing care beyond 100 days is not covered by Original Medicare.

What About Medigap?

Medicare Supplemental Insurance is known as Medigap. This is additional coverage you can purchase from a private insurance company that helps pay for your share of costs in Original Medicare (Medicare Part A and Part B). Overall, Medigap is designed to fill the coverage gaps of Original Medicare, and it helps cover coinsurance, deductibles, and copayments under Medicare Part A and Medicare Part B. Medigap policies are standardized, and there are 12 standardized Medigap Plans approved by the Federal Government: Plans A, B, C, D, F, F-High Deductible, G, G-High Deductible, K, L, M, and N. The benefits in each plan type are the same. For example, Plan F coverage is standardized across the board regardless of which private insurance company you buy the coverage from.

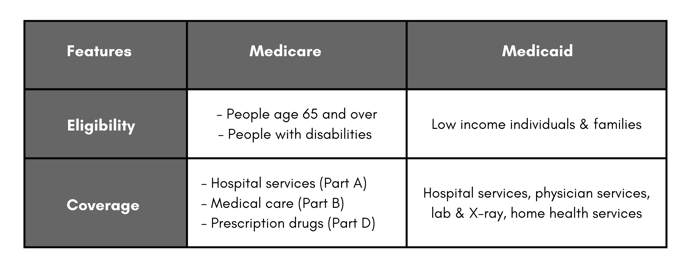

Medicare vs. Medicaid

Both established in 1965, Medicare and Medicaid are healthcare programs sponsored by the U.S. government that are designed to cover healthcare costs for American citizens. These programs are funded by taxpayers and have specific requirements for qualification and eligibility. Medicare offers medical coverage for Americans age 65 and older and for those with a disability, while Medicaid provides coverage for people with limited income and without access to other healthcare resources. Therein lies the primary difference between the two programs: Medicare has nothing to do with someone’s income level, whereas Medicaid has everything to do with a person’s income. You must qualify for Medicaid based on your financial status, while all Americans are eligible for Medicare once they turn age 65 or if they have a disability that qualified them for Medicare. Both of these programs are complex and multi-faceted. Let’s take a deeper dive into each below.

Click here to view & download the complete Medicare handout.

Questions and/or interested in how this applies to your financial life?

Email us here: info@afsfinancialgroup.com.